If you’re reading this, chances are you already know how it feels to sit at the kitchen table after the kids are in bed, staring at a bank statement and wondering how you’re going to make it all work. Maybe you’ve just come out of a relationship. Maybe you’ve been doing this on your own for years. Either way, you’re carrying a lot. And you’re doing it on one income.

Budgeting as a single mum in the UK isn’t the same as the generic money advice you find on most websites. You’re not a household with two salaries to fall back on. You’re managing childcare, school costs, bills, food, and your own sanity, often without anyone to split the load with. This single mum budget UK guide is written specifically for you.

In this post, you’ll learn:

- How to build a realistic single mum budget that actually works for UK living costs

- Which UK benefits and entitlements you might be missing out on

- Practical ways to reduce your biggest expenses without feeling deprived

- How to start saving even when money feels impossibly tight

Why Generic Budgeting Advice Doesn’t Work for Single Mums

Most budgeting content is written with a dual-income household in mind. You’ll see advice like “save 20% of your income” or “create an emergency fund of three months’ expenses”.

While those are fine principles in theory, they don’t account for the reality of what it actually costs to raise children alone in the UK right now.

Childcare alone can swallow an enormous chunk of your income. If your children are under school age, you might be looking at £1,200 to £1,800 a month for a full-time nursery place outside of London, and more in the south east.

Add in rent or a mortgage, food, school uniforms, after-school clubs, and the odd unexpected expense (because there’s always one), and the numbers look very different from the tidy budgets you see in personal finance magazines.

That’s the version of this I want you to have: the real numbers, not the tidy ones.

Why Generic Budgeting Advice Doesn’t Work for Single Mums

Most budgeting content is written with a dual-income household in mind. You’ll see advice like “save 20% of your income” or “create an emergency fund of three months’ expenses”.

While those are fine principles in theory, they don’t account for the reality of what it actually costs to raise children alone in the UK right now.

Childcare alone can swallow an enormous chunk of your income. If your children are under school age, you might be looking at £1,200 to £1,800 a month for a full-time nursery place outside of London, and more in the south east.

Add in rent or a mortgage, food, school uniforms, after-school clubs, and the odd unexpected expense (because there’s always one), and the numbers look very different from the tidy budgets you see in personal finance magazines.

That’s the version of this I want you to have: the real numbers, not the tidy ones.

Step One: Know Your Actual Numbers

Before you can budget properly, you need to know exactly what you’re working with. This means sitting down with your bank statements and going through the last two or three months in detail. I know it’s not a fun evening. But it’s the most important thing you can do.

Write down:

- Your total monthly income (wages, Child Benefit, Universal Credit, maintenance payments, any other income)

- Your fixed outgoings (rent or mortgage, council tax, energy, broadband, phone, car insurance, any subscriptions)

- Your variable spending (food, petrol or travel, clothing, kids’ activities, socialising)

- Any debt repayments (credit cards, loans, buy now pay later)

Once you can see it all laid out, you’ll know whether you’re in the red, barely breaking even, or have a small bit of breathing room.

Whatever the number is, knowing it is better than not knowing it. You can’t fix what you can’t see.

Which Budgeting Method Works Best?

There are several approaches to budgeting, but for single mums I’d generally recommend keeping it simple. The two methods that tend to work well are:

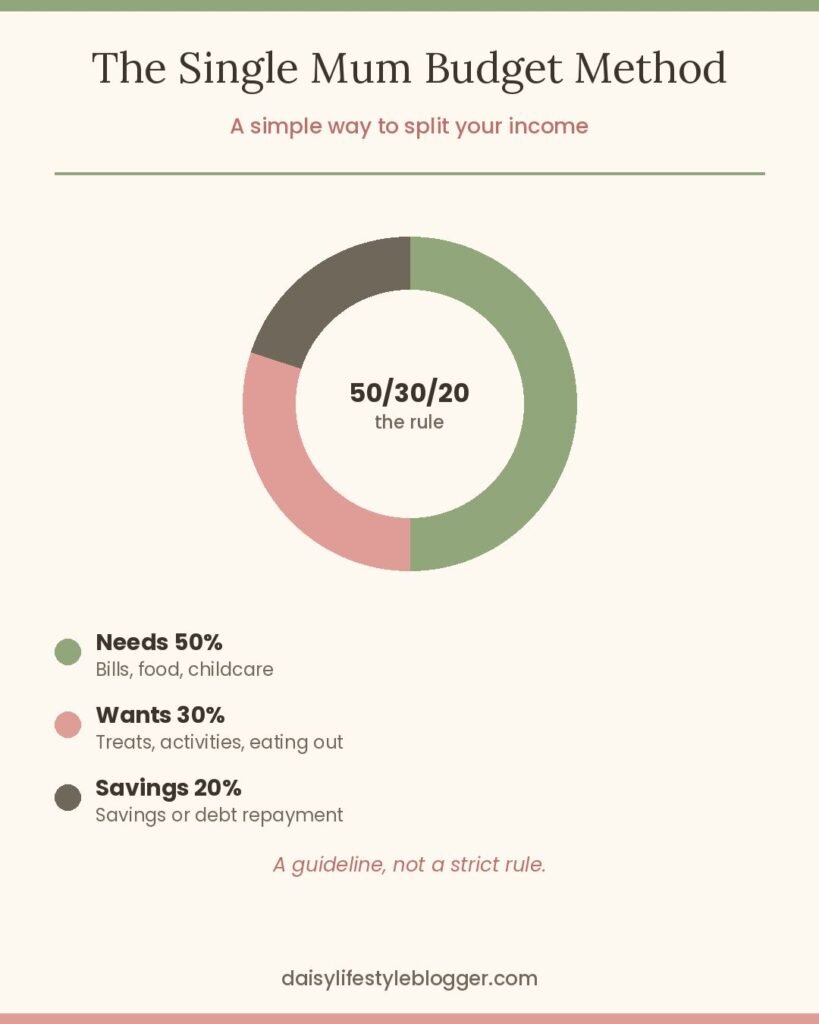

- The 50/30/20 rule: 50% of your income goes on needs (bills, food, childcare), 30% on wants (treats, activities, eating out), and 20% on savings or debt repayment. This is a guideline, not a strict rule. If childcare is eating 40% of your income right now, adjust accordingly.

- Zero-based budgeting: You assign every pound a job until your income minus your outgoings equals zero. This sounds intimidating, but it’s actually very freeing because nothing gets “lost” to vague spending.

Apps like Monzo or Starling Bank make zero-based budgeting much easier because you can create “pots” for different spending categories and move money into them on payday. It feels a bit like the old envelope method, but digital.

UK Benefits You Might Be Entitled To (And Might Not Know About)

This is one of the most important sections of this guide because in my experience, many single mums in the UK are not claiming everything they’re entitled to.

Whether it’s because the system is complicated, because they feel embarrassed, or because they simply don’t know it exists. Unclaimed benefits are money you’re leaving on the table.

Child Benefit

Child Benefit is paid to anyone responsible for raising a child under 16 (or under 20 if they stay in approved education or training). The current rate for 2026/27 is £27.05 per week for your first child and £17.90 for each additional child, with no limit on how many children you can claim for.

It is not means-tested if your income is under £60,000. So if you earn under that threshold, you should absolutely be claiming it.

One thing most people do not realise: as a single parent, you can ask HMRC to pay your Child Benefit weekly rather than the standard four-weekly. That can make a real difference to cash flow when you are managing everything on your own.

Just contact HMRC to request it.

Universal Credit

Universal Credit has replaced most of the older working-age benefits. If you’re on a low income, you may be entitled to a top-up even if you’re working. It’s not just for people who are out of work.

Also, Universal Credit includes a childcare element that can cover up to 85% of eligible childcare costs. If you haven’t looked into this, it’s worth doing so via the government’s own website or through Citizens Advice.

Free School Meals and the Healthy Start Scheme

If you’re on certain benefits, your children may be eligible for free school meals. In England, all children in Reception, Year 1, and Year 2 automatically receive free school meals regardless of income.

For children in Year 3 and above, the rules have genuinely changed for the better: from September 2026, every child in a household receiving Universal Credit qualifies for free school meals, whatever the household earns.

This replaces the old £7,400 household earnings cap that shut a lot of working single mums out before, and the Department for Education estimates it saves families around £495 a year per child.

If you were turned down in the past because you earned slightly too much, it’s worth applying again rather than assuming the old answer still stands.

I cover this in more detail, including the rules if you’re in Scotland, Wales or Northern Ireland, in Single Mum Grocery & Food Budget UK. The Healthy Start scheme also provides prepaid cards to help with the cost of fruit, vegetables, pulses, and milk if you’re pregnant or have a child under four and you’re on a qualifying benefit.

Council Tax Reduction

Single occupants automatically receive a 25% discount on council tax. If you’re on a low income, you may also qualify for a Council Tax Reduction through your local council, which can reduce your bill further, in some cases significantly.

Check your local council’s website or use the MoneySavingExpert benefits calculator to see what you might be entitled to.

Free Childcare Hours

This is one worth knowing about properly, because the rules changed significantly in September 2025. Eligible working parents in England can now access 30 hours of free childcare per week for children from nine months old right up to school age.

That covers 38 weeks of the year, in line with school terms. If you are not working or your income is below the threshold, you may still be entitled to 15 hours from when your child turns three.

Check your eligibility through the Childcare Choices website or your local council, and apply as early as you can because places fill up quickly.

Tackling Your Biggest Expenses

Once you know what you’re spending and you’ve checked your benefits, the next step is to look at where the biggest chunks of your money are going and find ways to reduce them without making your life miserable.

Food Shopping

Food is one of the most flexible parts of a budget. This means it’s also one of the easiest places to overspend without realising it.

Some practical strategies that work:

- Switch some of your shop to Aldi or Lidl. Their own-brand products are genuinely good, and the savings are real. You don’t have to do all of your shopping there, but even splitting your shop (basics from Aldi, specific things from Tesco or Sainsbury’s) can make a meaningful difference.

- Meal plan for the week. It sounds basic, but sitting down on a Sunday and planning your meals for the week dramatically reduces food waste and unplanned spending. Know what you’re buying before you walk into the shop.

- Use the Tesco Clubcard, Lidl Plus, and Morrisons More card. These loyalty schemes are genuinely worth it. The Tesco Clubcard, in particular, offers good discounts on staples.

- Check the reduced section. Most supermarkets mark down fresh food in the evening. It’s not glamorous, but it works.

I go into the full weekly breakdown by family size, including exact figures and which apps are actually worth your time, in Single Mum Grocery & Food Budget UK.

Energy Bills

Energy is a huge pressure point right now.

A few things that can help:

- The Warm Home Discount is a £150 annual rebate off your electricity bill. The 2025/26 scheme has now closed, but it reopens in October 2026, so add it to your diary now. Since 2025, the eligibility rules have been much broader: if you are on any qualifying means-tested benefit, including Universal Credit, you should receive it automatically without needing to apply. Your name does need to be on the energy bill, though. So if it is not, contact your supplier to sort that before October.

- Contact your energy supplier if you’re struggling to pay. They are legally required to help you with a payment plan and cannot cut you off without offering support first.

- Use a comparison site like MoneySavingExpert’s energy comparison tool to check whether you’re on the best available tariff.

Childcare Costs

I know from personal experience how childcare costs can feel like they swallow your entire salary whole, especially when your children are small.

On top of the free hours I have already mentioned, it is worth having a conversation with your employer about Tax-Free Childcare, which lets you pay into an account topped up by the government at a rate of 20p for every 80p you put in, up to £2,000 per child per year.

Also, some workplaces have emergency childcare schemes that not everyone knows to ask about. And if you are really struggling, Citizens Advice can tell you about local childcare bursaries that councils sometimes offer to single parents. It is always worth asking.

How to Start Saving When Money Is Already Tight

I know what you might be thinking: “Save? With what?” Bear with me.

The goal isn’t to save hundreds of pounds a month straight away. The goal is to build the habit and create even the smallest buffer.

So that when something unexpected happens (a car repair, a school trip, a broken washing machine), you’re not immediately in crisis.

The Help to Save Scheme

If you are on Universal Credit and earned at least £1 in your last monthly assessment period, you are eligible for the government’s Help to Save account.

You can save between £1 and £50 per month, and after two years, the government tops up your savings by 50%. Save £50 a month for two years (£1,200 in total), and you will receive a £600 bonus on top.

The scheme was originally due to close in 2025, but it’s being made permanent instead. From April 2028, it will also open up to UC claimants who get the child or caring element, even if they’re not currently working, which could bring in a lot more single mums who don’t qualify yet.

If you are eligible right now, open an account and start even with £5 or £10 a month. You only need to meet the eligibility rules when you open it.

Automate Your Savings

Even £10 or £20 a month into a separate savings pot on payday can make a difference over time. Monzo and Starling both let you set up automatic transfers into savings pots.

The key is to move the money before you have a chance to spend it.

Credit Unions

If you struggle to save because you’re tempted to dip into your savings, a credit union might be worth looking into. Think of them as community-run banks, not for profit, just there to help their members save and borrow affordably.

Some have savings accounts that make it harder to withdraw on a whim, which can actually be really useful if willpower is the issue.

Find one near you via the Association of British Credit Unions Limited (ABCUL) website.

Budgeting Isn’t Just About Spending Less: It’s About Earning More Too

There’s a limit to how much you can cut from a budget, especially when you already don’t have much to begin with. At some point, the most powerful thing you can do for your finances is find ways to bring more money in.

That doesn’t mean taking on a second job and running yourself into the ground.

It might mean:

- Selling things you no longer need on Facebook Marketplace, Vinted, or eBay

- Doing a few hours of freelance work during school hours or nap times

- Starting a small side project online, whether that’s self-publishing on Amazon KDP, setting up an Etsy shop, or affiliate marketing. I’ve done all three of these myself from my kitchen table around my daughter’s schedule, and they’re very much real options.

- Renting out a room in your home if you have a spare one (the Rent a Room scheme lets you earn up to £7,500 a year tax-free)

Your Single Mum Budget Template: A Simple Starting Framework

Here’s a simple framework you can adapt to your own situation. These percentages are a guide, not a rule.

| Category | Suggested % | Notes |

| Housing (rent/mortgage + council tax) | 30–35% | Including council tax single person discount |

| Food & household essentials | 12–15% | Meal plan and use Aldi/Lidl for staples |

| Childcare (after free hours) | 10–20% | Varies hugely by age and area |

| Transport | 8–10% | Car costs or public transport |

| Bills & utilities | 8–10% | Energy, broadband, phone |

| Children’s costs | 5–8% | Uniforms, clubs, school trips |

| Savings | 5–10% | Even £10/month matters — start small |

| Personal spending & treats | 5% | You deserve some |

| Emergency/unexpected | 3–5% | Build this up over time |

If your childcare costs are higher than this right now, don’t panic. It’s temporary. As children get older and into school, that money frees up. The goal is to plan for where you want to be, not just where you are.

If you want to see how these percentages actually play out for one, two, or three‑or‑more children, I’ve broken it down properly in Real Budget Breakdowns by Family Size UK.

And if you’d rather work from a ready-made printable than build your own spreadsheet, I’ve put together Free Budget Templates & Printables for Single Mums UK that you can start using today.

What to Do If You’re in Debt

Debt is incredibly common, and it carries a lot of shame that it absolutely does not deserve.

If you’re in debt (credit cards, loans, overdrafts, or buy now pay later balances), the first step is to get a clear picture of what you owe and to whom.

Don’t ignore it. Debt doesn’t go away, and it tends to get more expensive the longer it’s left.

There is free help available in the UK:

- StepChange Debt Charity offers free, confidential debt advice and can help you set up a Debt Management Plan

- Citizens Advice can provide local, in-person support and help you understand your options

- National Debtline has excellent online tools and a helpline

- MoneySavingExpert’s debt help section is one of the most comprehensive free resources available

Please ask for help. It is there, and it is free.

If your situation is more tangled than day-to-day debt, joint finances left over from a relationship, sorting out a will, guardianship for your children, or making sense of pensions, I go into all of that properly in Financial Advice & Planning for Single Mums in the UK.

Budgeting Around the School Calendar

One thing that catches a lot of single mums out is the school holiday squeeze. When term is in, childcare may be covered by school.

But during half-terms, summer holidays, Easter, and Christmas, your childcare costs can suddenly double or triple. And there are often extra costs on top, activities, days out, a new school uniform for September.

The best way to handle this is to plan for it in advance. Build a “school holiday fund” as a separate savings pot and put a small amount in each month, so you’re not scrambling every six weeks.

Also worth knowing: Holiday Activities and Food (HAF) programmes run by local councils offer free holiday clubs for children eligible for free school meals during Easter, summer, and sometimes Christmas holidays. Check with your council or school to see what’s available.

If affording days out or a proper break in the school holidays feels completely out of reach right now, it doesn’t have to be. I cover realistic, fully funded, and heavily discounted ways to do it in Single Mum Budget Travel UK.

Daisy’s Take 💛

I still remember the night I sat down and properly looked at my finances for the first time after my marriage ended. My daughter was in bed, the house was quiet, and I spread out three months of bank statements on the kitchen table. I didn’t cry — I think I was too exhausted for that — but I did feel completely overwhelmed. I had always earned good money. I had worked in property investment for years. And yet somehow, looking at those numbers on my own for the first time, I felt like a complete beginner.

What I wish someone had told me that night is exactly what I’ve written in this guide. That knowing your numbers, however scary they look, is the most powerful thing you can do. That there is help available that most people never claim. And that the goal isn’t perfection — it’s just getting a little more in control than you were yesterday.

You’re Already Doing the Hard Part

Budgeting as a single mum isn’t just about spreadsheets and cutting back. It’s about taking back a bit of control in a situation that can often feel overwhelming and uncertain.

The fact that you’re here, reading this, means you’re already taking it seriously, and that matters.

Start small. Know your numbers. Check every benefit you might be entitled to. Make one change this week, even if it’s a small one.

It adds up, I promise.

If you found this helpful, you might also want to read How to Save Money as a Single Mum UK. It goes deeper into specific cost-cutting strategies for food, energy, and kids’ expenses.

And if you’re thinking about ways to bring more money in, have a look at How to Make Money as a Single Mum UK.

What’s the one area of your budget that feels most out of control right now?

Frequently Asked Questions

What benefits am I entitled to as a single mum in the UK?

As a single mum in the UK, you may be entitled to Child Benefit, Universal Credit, a 25% council tax discount, free school meals, free childcare hours, and the Warm Home Discount, among others. Eligibility depends on your income and circumstances. The MoneySavingExpert benefits calculator and Citizens Advice are both good places to check what you’re entitled to.

How much should a single mum budget for food per week in the UK?

This depends on the size of your family, but a general guide is £50–£60 per week for a single mum with one child, shopping at a mix of Aldi or Lidl and a main supermarket. With a meal plan and a loyalty card, it is possible to keep costs lower. See my Single Mum Grocery & Food Budget UK post for a breakdown by family size.

How can I save money when I’m already struggling?

Start with the smallest possible amount, even £5 or £10 a month into a separate savings pot. The habit matters more than the amount at first. If you’re on Universal Credit and earning at least £1 a month, also look into the Help to Save government scheme, which gives you a 50% bonus on savings up to £50 per month.

Is it worth using a budgeting app as a single mum?

Yes, absolutely. Apps like Monzo and Starling Bank are particularly useful because they allow you to create separate “pots” for different spending categories and savings goals. This makes the envelope method digital and much easier to manage. Both are free to open and available in the UK.

What should I do if I’m in debt as a single mum?

The most important thing is not to ignore it. Free debt advice is available in the UK through StepChange, Citizens Advice, and National Debtline. They can help you understand your options, negotiate with creditors, and set up manageable repayment plans without charging you a penny. There is no shame in asking for help.